Retirement Spaghetti & Sequence Risk

Why an Hourly Plan Changes Everything for Retirement

Retirement Spaghetti & Sequence Risk: Why an Hourly Plan Changes Everything at Retirement

The final years before and the first years of retirement are the most financially vulnerable of your life. This period is when a sudden market downturn can permanently derail your long-term security.

If you are nearing or have just entered retirement, you likely have a complex array of accounts: Registered Retirement accounts, Tax Free accounts, as well as taxable investment accounts, and maybe a few old pension plans. We call this "Retirement Spaghetti."

While this confusion is annoying in your 40s and 50s, it becomes a major threat in retirement.

The Complexity of Scattered Assets

When your money is spread across multiple financial institutions, the sheer act of managing your retirement income stream becomes overwhelming:

Tax Chaos: You have different tax treatments for every account. Drawing $10,000 from one account might trigger a small tax bill, while drawing the same amount from another could push you into a higher tax bracket and even impact your eligibility for government benefits.

Inconsistent Strategies: Each account was likely opened under a different assumption or time period, leading to scattered investment strategies and accidental overlaps in holdings.

Administrative Overload: You waste valuable time chasing statements, updating passwords, and reconciling performance across five or six platforms just to get a clear picture of your total wealth.

This fragmented portfolio makes it nearly impossible to implement a strategic withdrawal plan that minimizes risk.

A Real Danger: Sequence of Returns Risk

In retirement, managing assets is fundamentally different than in your working years. Pre-retirement, volatility is your friend because it allows you to buy more shares cheaply (called dollar-cost averaging).

In retirement, volatility is not your friend. You now face Sequence of Returns Risk—the danger of being forced to withdraw money for living expenses during a year when the market is down.

When the market drops: If you are forced to sell assets to create an income stream, you lock in permanent losses. This depletes your principal faster, leaving less money to participate when the market eventually recovers.

The Solution: A Strategic Withdrawal Plan

A qualified Hourly CFP® professional focuses on helping you analyze these scattered accounts and create a unified strategy that protects your income.

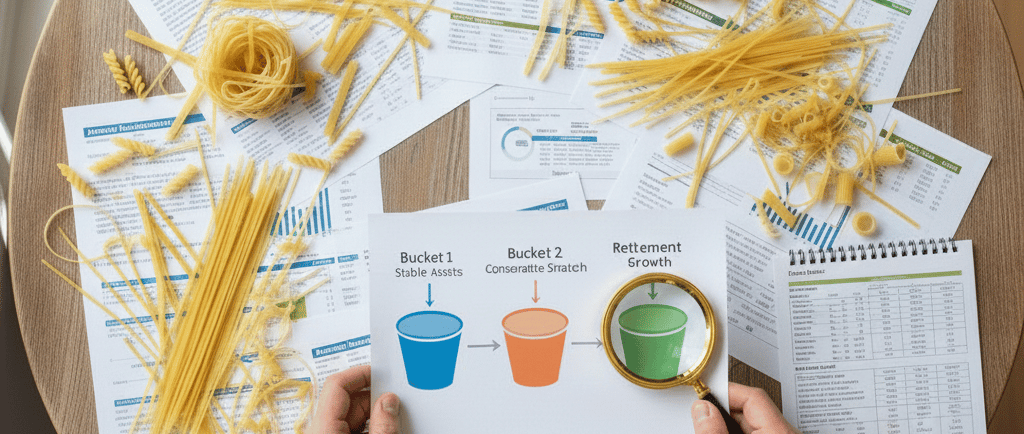

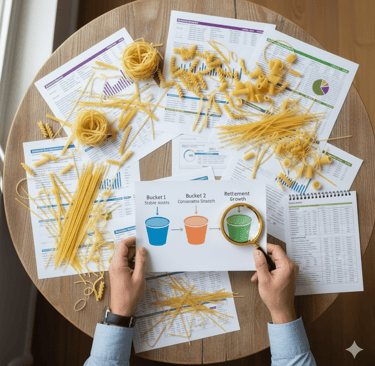

This strategy revolves around ensuring your redemptions are coming from assets that are relatively stable (if not 100% guaranteed) during market downturns. This often requires establishing a Withdrawal Bucket Strategy—a plan that divides your assets into three categories:

Bucket 1: Short-Term Income (1-5 years of living expenses): Held in highly stable assets (cash, fixed-income products, high-yield savings) so you can ride out market volatility for several years.

Bucket 2: Medium-Term Income (Years 4-7): Held in moderately conservative investments.

Bucket 3: Long-Term Growth (Years 5+): Held in growth-oriented investments that have time to recover from downturns.

How an Hourly Planning Session Solves the Spaghetti Problem:

You need to know which account to draw from first. Your hourly planner will:

Analyze Every Account: They evaluate all your scattered assets—taxable, tax-deferred, and tax-free—to determine the optimal order of withdrawals to minimize your lifetime tax burden.

Recommend Consolidation: They pinpoint which accounts can (and should) be consolidated to simplify management and facilitate the Bucket Strategy. Consolidation, when it makes sense, reduces fees and prevents the confusion that leads to poor withdrawal decisions.

Create a Roadmap: You walk away with a clear, step-by-step plan detailing where your money should be held and the specific order in which you should take distributions each year.

The Objective Difference

Your planner is paid by the hour to deliver this analysis and strategic roadmap. They have no incentive to recommend selling off a low-cost, high-performing account just to move the money into one they manage.

If you are at or near retirement, it’s time to move past the confusion of "Retirement Spaghetti." Gain clarity now to protect your assets from unnecessary losses later.

Use our simple form today to Find Your CFP® Match and get the unbiased plan you need.